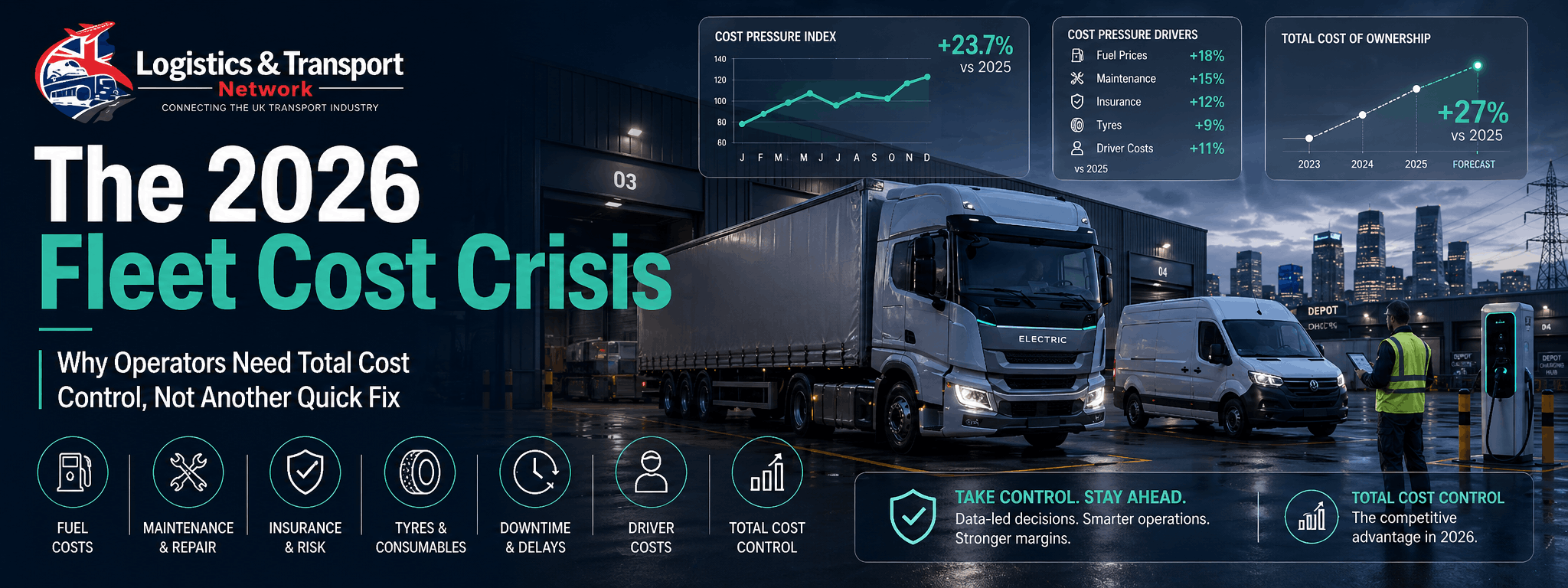

Multiple cost lines are rising at the same time, squeezing margins across UK logistics and transport. Here’s what is really driving the pressure — and the practical steps operators can take now with supplier support to regain control.

UK fleet operators are facing one of the most challenging cost environments in recent years.

Fuel and energy costs remain volatile. Maintenance and repair bills continue to rise. Insurance renewals are becoming more forensic. Tyres, parts and consumables are adding pressure. Driver-related costs remain difficult to manage. Vehicle replacement decisions are becoming more complex as operators balance ageing diesel assets, higher purchase prices and the transition towards electric vehicles.

The result is not one single crisis.

It is the cumulative effect of multiple cost lines moving against operators at the same time.

Many fleet managers and transport directors describe the pressure as “death by a thousand cuts”. No single cost increase is necessarily enough to break the operating model on its own, but together they are quietly eroding margins, weakening cash flow and making it harder to plan with confidence.

This is why 2026 needs a different approach.

Operators cannot solve a multi-cost problem with isolated fixes.

The fleets that regain control will not simply be those that chase cheaper fuel, delay replacement vehicles or renegotiate insurance at the last minute. They will be the operators that build a connected view of fuel, maintenance, downtime, insurance, tyres, driver performance, compliance and whole-life vehicle cost.

This is not about cutting corners.

It is about building better cost intelligence, using data earlier, working with the right suppliers and moving from reactive firefighting to proactive total cost control.

The good news is that operators are not facing this alone.

Across the supplier market, practical solutions are already helping fleets reduce waste, prevent downtime, improve driver behaviour, strengthen insurance evidence, manage tyre and maintenance costs, and make smarter vehicle investment decisions.

The challenge for 2026 is knowing where to focus first.

What Is Driving the 2026 Fleet Cost Crisis?

The current cost pressure is not coming from one direction.

It is being driven by several forces at once.

Fuel and Energy Volatility

Fuel remains one of the largest and most unpredictable cost lines for fleet operators. Even where prices stabilise for a period, sudden movements in oil markets, geopolitical disruption, currency changes or supply interruptions can quickly affect pump prices and contract costs.

For high-mileage fleets, even small movements in fuel prices can create significant budget pressure.

At the same time, operators planning for electric vehicles are having to think more carefully about electricity costs, charging tariffs, depot energy capacity and how future fleet charging will be managed.

Fuel strategy and energy strategy are now increasingly connected.

Maintenance, Repair and Parts Inflation

Maintenance and repair costs have become harder to control.

Parts prices have risen. Vehicle technology is becoming more complex. Repair lead times can be longer. Some operators are extending vehicle lifecycles due to replacement costs, but older vehicles can increase breakdown risk, inspection pressure and workshop demand.

This creates a difficult balance.

Replacing vehicles can be expensive, but sweating assets for too long can increase maintenance spend, downtime and compliance risk.

Insurance and Claims Inflation

Fleet insurance is also under pressure.

Insurers are looking more closely at claims history, repair costs, vehicle downtime, driver behaviour, theft risk, camera evidence, telematics data and the strength of an operator’s risk controls.

For operators, this means insurance is no longer simply an annual renewal exercise.

It is becoming a risk-management conversation.

The fleets that can evidence strong safety culture, driver monitoring, claims control, vehicle technology and proactive risk reduction are better placed to have constructive renewal discussions.

Those who cannot may face tougher questions, higher premiums or reduced flexibility.

Tyres, Parts and Consumables

Tyres, parts, AdBlue, lubricants and other consumables rarely dominate boardroom conversations, but they matter.

When costs increase across multiple small categories, the combined impact can become significant.

Poor tyre management, inefficient procurement, inconsistent pressure monitoring, premature wear and unplanned replacements can all add avoidable costs.

In a tight-margin environment, these details matter more.

Driver Costs, Productivity and Retention

Driver-related costs remain a major pressure for many operators.

Recruitment, training, overtime, agency cover, absence, retention and productivity all affect total fleet cost.

Driver behaviour also has a direct impact on fuel usage, tyre wear, maintenance, accident risk and insurance claims.

This means driver performance is no longer just an HR or operational issue.

It is a cost-control issue.

Vehicle Replacement and Transition Pressure

Vehicle replacement decisions are becoming more difficult.

Operators are balancing higher purchase prices, uncertain residual values, emissions requirements, clean air zone considerations, EV transition planning, charging infrastructure costs and whole-life cost modelling.

Some are delaying replacement to preserve cash. Others are accelerating change to improve efficiency or meet customer expectations.

Both routes carry risk if the decision is not based on clear data.

This is why the total cost of ownership is becoming central to fleet strategy.

Why This Cost Pressure Feels Different

Fleet operators have faced cost spikes before.

But the current environment feels different because the pressure is multi-dimensional.

Fuel, maintenance, insurance, tyres, drivers, downtime, and vehicle replacement are all connected. A decision in one area can create consequences somewhere else.

For example:

- Delaying vehicle replacement may reduce short-term capital spend but increase maintenance and downtime.

- Cutting driver training may save money initially, but increases fuel use, claims risk and tyre wear.

- Choosing the cheapest maintenance route may create higher failure rates later.

- Ignoring telematics data may mean missing fuel waste, harsh driving patterns or early vehicle health warnings.

- Leaving insurance preparation until renewal may weaken the operator’s ability to evidence risk control.

The issue is not just that costs are rising.

It is that many fleets still manage cost lines in silos.

Fuel is reviewed separately from driver behaviour. Maintenance is reviewed separately from downtime. Insurance is reviewed separately from claims evidence. Vehicle replacement is reviewed separately from whole-life operating cost.

That fragmented approach is becoming too expensive.

In 2026, operators need a more connected model.

The Hidden Cost: Downtime

One of the most damaging cost pressures is not always visible on the invoice.

Downtime.

When a vehicle is off the road, the operator is not only paying for the repair.

They may also face missed delivery windows, replacement vehicle costs, driver disruption, overtime, reduced route capacity, customer penalties, service failures and reputational damage.

In some cases, downtime can cost far more than the repair itself.

This is why predictive maintenance, vehicle health monitoring, faster repair pathways, parts planning and better workshop scheduling are becoming central to fleet cost control.

The strongest operators are not just asking:

“How much does this repair cost?”

They are asking:

“How do we prevent this vehicle from being off the road in the first place?”

That shift matters.

A fleet that can identify faults earlier, plan maintenance better and reduce unplanned failures has a clear operational advantage.

Insurance Is Now a Risk-Management Conversation

Insurance is often treated as something that happens once a year.

That approach is no longer enough.

As claims costs, repair inflation, and vehicle complexity continue to affect the market, insurers are becoming more interested in the quality of the operator’s risk management.

This includes:

- Claims history

- Driver behaviour

- Telematics evidence

- Camera systems

- Incident reporting

- Driver training

- Vehicle maintenance records

- Theft prevention

- Route risk

- EV and alternative fuel risk

- Repair and downtime management

Operators that can present clear evidence of proactive risk control may be better placed to influence renewal conversations.

That does not mean premiums will automatically fall.

But it does mean the operator is moving into the renewal discussion with stronger evidence, better data and a clearer risk story.

For fleets under cost pressure, that matters.

Insurance is no longer just about buying cover.

It is about proving that the business is a well-managed risk.

Vehicle Replacement Decisions Are Getting Harder

A major challenge for 2026 is deciding when to replace vehicles and what to replace them with.

Many operators are trying to extend asset life because new vehicles are expensive. But older vehicles can bring higher maintenance costs, greater downtime risk, weaker fuel efficiency and increased compliance pressure.

At the same time, the transition to electric and alternative fuel vehicles is changing the replacement conversation.

Operators now need to consider:

- Purchase price

- Funding and leasing options

- Residual values

- Fuel or energy costs

- Maintenance profile

- Downtime risk

- Charging or refuelling infrastructure

- Clean air zone exposure

- Customer requirements

- Carbon reporting

- Driver suitability

- Payload and route requirements

A simple purchase-price comparison is no longer enough.

The real question is whole-life cost.

This is where fleet finance partners, leasing providers, TCO platforms, EV transition specialists and asset management consultants can help operators make better decisions.

The goal is not to replace everything quickly.

It is to understand which vehicles are costing too much to keep, which should be retained, and where new technology or different funding models could create long-term value.

Data Is the Difference Between Pressure and Control

Operators cannot control every external cost.

They cannot control global oil markets. They cannot control every insurance market movement. They cannot control every parts price increase or vehicle supply issue.

But they can control how quickly they see cost movement, identify waste and intervene.

That is where data becomes critical.

Fuel data, telematics, maintenance records, tyre monitoring, claims history, driver behaviour, route performance, workshop records and vehicle utilisation all tell part of the story.

The real value comes when those data points are connected.

A vehicle with poor fuel performance may also show harsh driving patterns. A driver with repeated incidents may also be increasing tyre and maintenance costs. A depot with frequent breakdowns may have a maintenance planning issue. A route with high fuel use may need review. A vehicle with rising repair costs may be approaching the wrong side of its whole-life cost curve.

Without data, operators see the cost after it has happened.

With better visibility, they can act earlier.

This is the shift from cost reporting to cost control.

Current and Future Impacts for UK Operators

Right Now

In 2026, many operators are already feeling the pressure.

Budgets are harder to forecast. Repairs are more expensive. Vehicles are staying off the road for longer. Insurance renewals require more preparation. Driver-related costs remain stubborn. Fuel volatility continues to make planning difficult.

For some fleets, the most frustrating part is the limited ability to pass all costs on to customers.

Freight rates, customer contracts and competitive pressure often mean operators absorb increases rather than recover them fully.

That is why internal cost control has become so important.

When external pricing power is limited, operational efficiency becomes the margin defence.

Looking Ahead

Over 2027 and 2028, the gap between proactive and reactive operators is likely to widen.

Operators that invest in connected cost management may benefit from:

- Better fuel efficiency

- Fewer unplanned breakdowns

- Lower downtime exposure

- Stronger insurance renewal evidence

- Improved driver performance

- Better tyre and maintenance control

- More accurate vehicle replacement decisions

- Stronger cash flow planning

- More competitive customer pricing

Operators who delay may face:

- Continued margin erosion

- Higher repair and downtime costs

- Weaker insurance renewal positions

- Ageing fleet risk

- Reduced operational flexibility

- Poorer visibility over true cost performance

The pressure is real, but so is the opportunity to improve.

Your 2026 Fleet Cost Control Action Plan

The strongest response is not to attack every cost at once.

It is to identify where the greatest pressure sits, where the fastest gains are possible, and which supplier-supported interventions can deliver measurable value.

Phase 1: Build a True Cost Picture

Start by creating a clear breakdown of fleet cost across the main categories:

- Fuel and energy

- Maintenance and repair

- Tyres

- Insurance and claims

- Driver-related costs

- Downtime

- Vehicle finance and depreciation

- Compliance costs

- Replacement vehicle costs

- Route and utilisation efficiency

Operators should identify the top three to five cost drivers having the biggest impact on margin.

This should include both direct costs and hidden costs.

A low repair bill may still be expensive if the vehicle was off the road for three days.

A cheap tyre strategy may not be cheap if it increases replacements, fuel use or breakdown risk.

A low insurance premium may not represent good value if claims support and downtime management are weak.

The aim is to understand true cost, not just invoice cost.

Phase 2: Prioritise High-Impact Interventions

Once the cost picture is clear, operators should focus on interventions that can deliver the fastest and most measurable impact.

This may include:

- Fuel efficiency programmes

- Route optimisation

- Driver behaviour coaching

- Telematics review

- Predictive maintenance

- Tyre pressure and wear monitoring

- Claims management improvement

- Insurance risk evidence preparation

- Workshop scheduling

- Parts procurement review

- Vehicle utilisation analysis

The priority should be areas where cost is high, data is available and supplier solutions can produce measurable improvement.

Not every project needs to be complex.

In many fleets, small operational changes across fuel, tyres, driver behaviour and maintenance can produce meaningful savings.

Phase 3: Strengthen Insurance and Risk Evidence

Operators should prepare for insurance renewal long before the renewal date.

This means building an evidence pack that shows:

- Claims trends and corrective actions

- Driver training activity

- Telematics and camera use

- Maintenance standards

- Incident reporting processes

- Theft prevention measures

- Safety technology investment

- Route and depot risk controls

- Actions taken to reduce repeat claims

This helps move the conversation from price-only renewal to risk quality.

Insurance brokers, risk management specialists, telematics providers, camera suppliers and driver training partners can all support this process.

The goal is to give insurers confidence that the fleet is being actively managed.

Phase 4: Reduce Downtime Before It Happens

Downtime needs to be treated as a controllable cost.

Operators should review:

- Breakdown history

- Common failure points

- Vehicle age and mileage

- Maintenance intervals

- Parts availability

- Workshop capacity

- Driver defect reporting

- Vehicle health data

- Recovery and replacement arrangements

Predictive maintenance tools, fleet management platforms and workshop partners can help operators identify risks earlier and plan interventions before failures become operational disruption.

Reducing downtime is one of the most direct ways to protect service, revenue and customer confidence.

Phase 5: Reassess Whole-Life Vehicle Cost

Replacement decisions should be based on whole-life cost rather than age alone.

Operators should assess:

- Repair cost trends

- Fuel efficiency

- Downtime frequency

- Compliance risk

- Driver suitability

- Emissions exposure

- Residual value

- Finance options

- EV or alternative fuel suitability

- Charging or refuelling implications

This allows fleets to make clearer decisions about which vehicles to retain, replace, repower, electrify or reallocate.

A vehicle may appear cheaper to keep, but if it is causing downtime, poor fuel performance and rising repair bills, the true cost may tell a different story.

Phase 6: Monitor, Review and Improve Continuously

Cost control is not a one-off exercise.

Operators should create regular reporting that tracks the key indicators:

- Fuel use per vehicle, driver or route

- Maintenance cost per mile

- Tyre cost per mile

- Downtime hours

- Claims frequency and cost

- Driver behaviour scores

- Vehicle utilisation

- Cost per delivery, route or contract

- Whole-life cost by vehicle type

This gives operators the ability to spot patterns, intervene earlier and measure whether supplier-supported solutions are delivering the expected return.

The best fleets will not simply react to cost increases.

They will build a rhythm of continuous cost improvement.

How Suppliers Are Helping Operators Fight Back

The supplier community has responded strongly to the cost challenge.

The most valuable providers are no longer just selling products or services in isolation. They are helping operators solve specific cost problems with measurable outcomes.

Fuel Management and Route Optimisation Providers

Fuel cards, telematics platforms and route optimisation tools can help operators reduce unnecessary mileage, idling, inefficient driving and poor route planning.

Even small percentage improvements can make a material difference across high-mileage fleets.

Telematics and Driver Behaviour Platforms

Telematics gives operators visibility over harsh braking, acceleration, speeding, idling, route efficiency and vehicle utilisation.

When combined with driver coaching, this can reduce fuel use, tyre wear, accident risk and maintenance stress.

Predictive Maintenance and Vehicle Health Tools

Predictive maintenance platforms help operators spot issues earlier, reduce unplanned breakdowns and extend component life.

This is particularly valuable where downtime is one of the highest hidden costs.

Insurance Brokers and Risk Management Specialists

Fleet insurance partners are increasingly helping operators prepare stronger renewal evidence, analyse claims data, improve driver risk controls and present a better risk story to insurers.

Camera, Safety and Incident Technology Providers

Dashcams, AI cameras, proximity sensors and safety systems can help reduce incidents, support claims defence, improve driver behaviour and provide stronger evidence where liability is disputed.

Tyre and Asset Management Partners

Tyre monitoring, pressure management, procurement support and lifecycle analysis can help operators reduce avoidable tyre spend, improve fuel efficiency and minimise breakdown risk.

Fleet Finance, Leasing and TCO Specialists

Finance and leasing partners can help operators assess whole-life cost, replacement timing, EV transition options and the most suitable funding model.

Driver Training and Wellbeing Providers

Training, fatigue management, wellbeing tools and driver engagement support can help reduce incidents, improve retention and support better performance behind the wheel.

Fleet Management and Cost Analytics Platforms

These platforms bring multiple cost lines together, helping operators see the real relationship between fuel, maintenance, tyres, downtime, claims and vehicle utilisation.

The most useful supplier relationships in 2026 will be those that help operators prove impact.

Not just activity.

Not just visibility.

Impact.

Real Momentum Is Building

Across the UK fleet and logistics sector, the conversation is changing.

Operators are increasingly looking beyond one-off savings and towards a more connected view of cost control.

Fleet managers, transport directors, finance teams and operations leaders are asking sharper questions:

Where are costs rising fastest?

Which vehicles are costing too much to keep?

Which routes are inefficient?

Which drivers need support?

Which claims are repeatable?

Which suppliers can prove savings?

Which investments will pay back quickly?

Where is downtime quietly damaging margin?

These are not theoretical questions.

They are now central to operational resilience and profitability.

The positive news is that operators do not need to solve everything at once.

A structured approach, supported by the right suppliers, can quickly identify where the greatest savings and resilience gains are likely to come from.

The Bottom Line

The 2026 fleet cost crisis is real.

But it is not uncontrollable.

The operators who will be strongest over the next two years are those who stop treating cost lines in isolation and start building a connected cost-control strategy.

That means understanding fuel, maintenance, tyres, insurance, downtime, driver behaviour and vehicle replacement as part of one operating model.

It also means working with suppliers who can deliver practical, measurable improvements.

The goal is not to cut corners.

The goal is to protect margin, improve resilience and build a fleet operation that can perform in a tougher cost environment.

The fleets that act now will be better placed to control spend, reduce disruption and compete with confidence.

Join the Fleet Cost Control Series

To support operators through this period of rising fleet cost pressure, the Logistics & Transport Network will be developing a focused Fleet Cost Control Series.

The series will help UK fleet, logistics and transport operators understand:

- How to identify the true cost drivers across their fleet

- How fuel efficiency, route optimisation and driver behaviour can protect margins

- Why downtime is one of the most important hidden costs to reduce

- How maintenance, tyre and asset management can improve whole-life value

- Why insurance renewal preparation now depends on stronger risk evidence

- How fleet finance, leasing and TCO modelling can support better replacement decisions

- Which supplier partners are actively helping operators deliver measurable cost improvements

This series is designed to give operators practical guidance, supplier insight and a clearer route through the decisions that need to be made now.

To enrol your organisation or register interest in receiving the series, email:

Fleet cost pressure may be here to stay, but with the right data, planning and supplier support, UK operators can move from reactive cost control to stronger, smarter and more resilient fleet performance.